The headlines can be startling:

"Alleged failure to diagnose pneumonia results in a bilateral below-the-knee amputation.”

“Alleged failure to communicate pathology report addendum to surgeon resulting in death of married male.”

“Alleged negligent use of electrocautery during surgery ignites fire, resulting in burns to the face and neck of patient.”

But headlines only cover the tip of the iceberg when it comes to the total cost of risk for a hospital or healthcare practice. And if recent events—an economic downturn, the global pandemic, business interruption, and the contentiousness of the current elections—have taught us anything, it is that risks and perils that exist outside of the delivery of medical care have a material impact on the business of

medicine and the people who work in it.

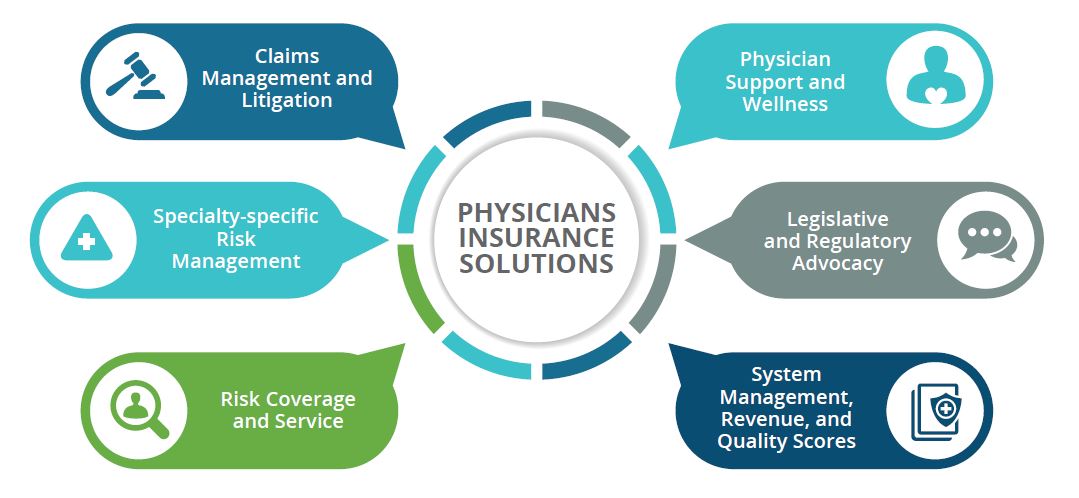

When working with today’s physician practices and hospitals/systems, Physicians Insurance believes the best place to start is to consider six macro-elements that impact an organization’s costs, regardless of size. These six key areas are: risk coverage related to the delivery of care (e.g., your medical or hospital professional liability policy); costs associated with risk-mitigation activities, processes, and education; claims management and litigation for when a claim or trial occurs; physician and care-team support and wellness programs to restore the resiliency of providers and minimize burnout; governmental relations and the host of activities around advocacy for the protection of physicians and care providers; and services around the business of medicine, which include everything from quality scores to bundled payment programs, employment practices, HIPAA compliance, and revenue management.

• Risk Coverage and Services: This is the keystone to a good risk-financing program. You’re basically buying coverages that will protect you when something happens. A good, comprehensive program is one that includes coverage for both direct patient treatment and for vicarious liability for the conduct of other insured parties, and may include general liability, employment-practices liability, cyber liability, and directors and officers/management liability. You want to be sure that the coverage limits and any endorsements (add-ons or exclusions) provide the right amount of coverage for your needs. It’s just as possible to be over-insured as it is to be under-insured, and your premiums are largely based on what coverages you’re buying and your history of losses in those areas.

Insurance markets historically go through somewhat predictable cycles, which influence insurance limits and corresponding premium. A soft market is characterized by abundant capacity, ample competition, and low premium due to decreases in claims frequency and severity. Soft markets are followed by hard markets where capacity diminishes, competition lessens, and premium increases to match changes in claims frequency and severity. Nationally as well as in the Pacific Northwest, there is an ongoing uptrend in the frequency and severity of claims and suits. This suggests that the medical professional liability industry is in a hardening market.

Additionally, when you negotiate your policy terms, be sure to consider the trade-offs of premium and deductibles, and any key reporting timelines. All of these items matter and will impact your overall expenses.

• Specialty-specific Risk Management: Risk-management and risk-mitigation services are designed to mitigate risks while lowering your costs. Without targeted and customized actions in your practice, hospital, or care setting, other people's claims and litigation headlines can quickly become your own. The goal is to find services that compliment your existing programs or efforts, maybe take you to the next level of sophistication, and do so in a manner that is sustainable. Most insurance companies will have some type of risk-management services or products, but not all programs are the same.

• Specialty-specific Risk Management: Risk-management and risk-mitigation services are designed to mitigate risks while lowering your costs. Without targeted and customized actions in your practice, hospital, or care setting, other people's claims and litigation headlines can quickly become your own. The goal is to find services that compliment your existing programs or efforts, maybe take you to the next level of sophistication, and do so in a manner that is sustainable. Most insurance companies will have some type of risk-management services or products, but not all programs are the same.

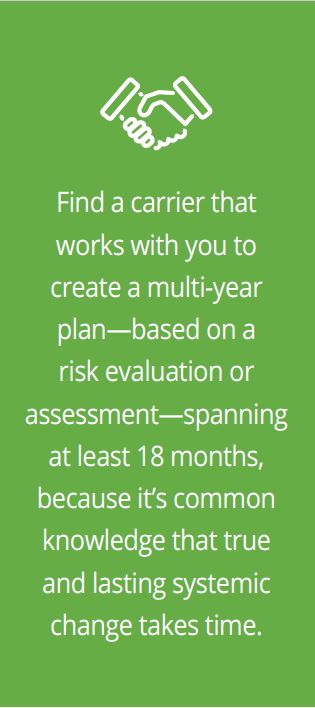

Find a carrier that works with you to create a plan that can evolve over time—based on a risk evaluation or assessment—spanning at least 18 months, because it’s common knowledge that true and lasting systemic change takes time. You’re going to also want access to continuing education (some accredited, some simply good information) that is relevant to both your setting and contemporary practices.

Accessing these services and education on your own in the retail market could cost tens of thousands of dollars, depending on your size and the complexity of the program. So ensuring it’s part of and included with your underlying policy could be an important cost savings to you.

• Claims Management and Litigation: Claims happen—it’s not a matter of if but when. So right up there in importance with a good underlying policy is having a claims team with a proven track record of defending physicians and hospitals, for whenever that policy may be needed. Look for a carrier with a claims team who understands that this could be the most difficult experience of your professional life, and who will be there for you when you need them. Some claims teams are understaffed, which means they handle a lot of cases and spend only a little bit of time on each—or the insurance company may be publicly traded, which may mean that their incentive is often to settle as early as possible for as little as possible. Make sure you find an insurance carrier that matches your own philosophy or has consent to settle as part of the language in the policy.

• Physician Support and Wellness: Claims administration is part of the policy you’ve purchased. But support services or other important services are not always included, and could cost you thousands more if you were to purchase them yourself in an already stressful time of need.

Another benefit of some carriers is litigation support for policyholders. This often takes the form of a psychologist or psychiatrist who can support the defending physician during litigation, or perhaps a peer-support program in which other physicians who have had similar experiences can walk alongside someone going through a claim or litigation experience for the first time. These support programs can sometimes extend to the entire care team involved in an incident or adverse outcome. Other complimentary programs could cover burnout, caregiver suicide prevention, and substance abuse.

Physicians Insurance is the only carrier in the Northwest to offer individualized and “in-the-moment” comprehensive physician/clinician-support programs, which are designed to keep physicians engaged, avoid further complications or errors, and preclude the costs of lost productivity and new-physician recruitment.

• Legislative and Regulatory Advocacy: Some risks that physicians and hospitals face don’t originate in the exam or operating room, but in legislative chambers. Not all insurance carriers dedicate resources to protecting their members at the state and national levels, and for you to engage in these activities on your own could create unsupportable costs for your organization. Physicians Insurance believes that it’s part of our mission to support comprehensive effective legislation that enhances the healthcare liability system, promotes meaningful patient-safety initiatives, improves healthcare quality, and supports communication between healthcare professionals, providers, and patients.

That’s why Physicians Insurance is the only medical professional liability carrier based in the Northwest with an in-house lobbyist registered in Oregon and Washington, who focuses on protecting members from legislation negatively impacting the care and business of medicine, and on providing advocacy on challenges to medical professional liability that may (1) create new causes of action, (2) alter the standard of care, (3) establish strict liability for providing or not providing care, or (4) impose onerous or unnecessary duties on healthcare professionals and providers.

That’s why Physicians Insurance is the only medical professional liability carrier based in the Northwest with an in-house lobbyist registered in Oregon and Washington, who focuses on protecting members from legislation negatively impacting the care and business of medicine, and on providing advocacy on challenges to medical professional liability that may (1) create new causes of action, (2) alter the standard of care, (3) establish strict liability for providing or not providing care, or (4) impose onerous or unnecessary duties on healthcare professionals and providers.

As you consider your total cost of risk, consider how this upstream effort impacts the downstream care you’re able to provide your community and patients, and how the legislative environment itself might make it easier or harder for you to run your healthcare business.

• System Management, Revenue, and Quality Scores: While other services that may surround your policy are designed to mitigate risks and lower costs, another area of risk that’s often overlooked is protecting your revenue and ability to conduct your business.

Part of protecting your own risks is ensuring you have access to vendors, partners, and information that support optimizing your revenue and expense management, including clinical and practice improvement reviews, physician compensation analysis, revenue cycle management, real-estate development and analysis, patient-satisfaction score analysis and improvement, data acquisition and analysis services, and cyber/privacy tool-sets to protect you and your patients.

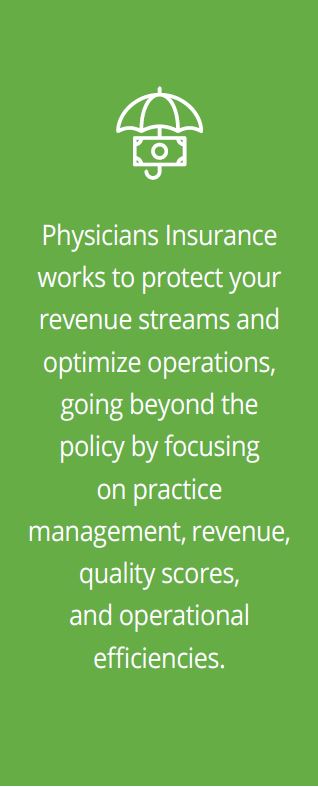

Access to these services individually can cost tens of thousands of dollars for each—but they’re sometimes made available at a discount, or even at no cost, through your carrier. Through exclusive partnerships and other licensing arrangements, Physicians Insurance works to protect your revenue streams and optimize operations, going beyond the policy by focusing on practice management, revenue, quality scores, and operational efficiencies.

COMPREHENSIVE VIEW OF RISK

Providing comprehensive solutions goes well beyond just offering a policy to cover professional liability. In today’s healthcare environment, your practice or hospital also needs to focus on the other elements that directly impact your business operations and the wellness of your team. These are specific resources that help to mitigate risks and decrease severity in both outpatient and inpatient settings, improve patient safety and quality scores, and build care-team resilience. It’s this approach that has made Physicians Insurance the largest medical and hospital professional liability carrier in the Pacific Northwest—and it’s a philosophy central to our mutual-company identity that puts relationships, communities, and our members’ needs first in all that we do.